Below are four articles regarding estate planning. How assets are passed to heirs.What are estate documents.Why estate documents are needed. Using trusts in your estate plan.

Most federal employees probably know that means it is time to check whether their Federal Employees Health Benefit (FEHB) Program health insurance plan is the best for their needs and to also check whether enrolling in a second federal benefits program, the Federal Employees Dental and Vision Insurance Program (FEDVIP), makes sense.

But there is a third benefit federal employees should be evaluating each Open Season and may not be: the Federal Flexible Spending Account Program (FSAFEDS), a federal benefits program that can reduce tax bills by using pretax dollars to pay for health and dependent care out-of-pocket expenses.

SEE MORE

Transitioning from full-time employment to retirement is not just a significant lifestyle change but requires a shift from saving and accumulating wealth to spending those hard-earned dollars to fund retirement. Part of the transition requires making important financial decisions, which can have a significant impact on your long-term wealth.

This article addresses 10 of the key decisions to consider, including Social Security timing, rolling your TSP into an IRA, streamlining your financial life, and taking the appropriate amount of risk.

A fee-only, trusted advisor, who looks out for your best interests and is there for you when retirement presents its challenges, can be invaluable. Sometimes an advisor’s biggest role is preventing one from making an irreversible mistake. (ClearLogic is a fee-only, fiduciary advisor.)

SEE MORE

Federal employees, whether CSRS or FERS, have many decisions – some of which are irrevocable – to make as they complete their retirement paperwork. (With almost half of our clients federal employees and retirees, ClearLogic guides federal employees in making the right decisions to optimize their retirement.)

Key decisions to make include: choosing their survivorship option, considering a partial rollover of your TSP, investing in the voluntary contribution plan, declining Medicare Part B, electing the 75% reduction paid up FEGLI option for life insurance, banking your sick pay leave payout, and selecting the best day of the month to retire (especially for CSRS).

These are 7 tips for federal retirement. (Because other decisions for retirement can vary, ClearLogic analyzes these based on individual specific circumstances.)

SEE MORE

Federal retirees with healthy retirement incomes are in a unique position when it comes to health insurance.

On the surface, Medicare Part B appears attractive, because you most likely will not incur any co-pays or co-insurance costs with your Federal Employee Health Benefit [FEHB] plan. Unlike Medicare Part A which is free, Medicare Part B premiums are significant – for an individual with an adjusted gross income just over $85,000 per year are $2,250 per year and for a married couple just over $170,000 are $4,500. Keep in mind the FEHB plan covers 100% of medical expenses once the annual out-of-pocket maximum is reached – typically $5,000 for an individual and $10,000 for a couple.

In most cases even with periodic, major medical expenses, carrying Medicare Part B in addition to an FEHB plan will cost more than it will save you in out-of-pocket costs. There are a few cases where the cost of carrying Medicare Part B more than pays for itself. It all depends on your individual circumstances.

SEE MORE

The Office of Government Ethics requires federal employees to annually submit a Confidential Financial Disclosure Report (Form 450) each year before February 15.

Federal News Network sat down with Shawn Steel, a certified financial planner with ClearLogic Financial, to learn how this can affect federal employees’ retirement plans and what they need to consider when investing.

SEE MORE

We often (maybe too often) beat the drums about staying the course and thinking long-term. We recommend this article; in which, Barry Ritholtz eloquently justifies several of ClearLogic’s Investment Principles regarding long-term thinking.

Here are a few of our favorite quotes from the article:

- “investors spend too much time worrying about risks that are either statistically unlikely or,

conversely, the kind of risk that ends up being good for their portfolios over the long haul.” - “over the past century, U.S. stocks have returned about 10 times what Treasurys have,

although they also experienced numerous massive selloffs over that time” - “Politics and investing don’t mix…How does knowing the political party of a president impact

a portfolio if a portfolio will outlast the administration? People who make decisions out

of fear or politics miss out.”

There will be market corrections, some significant. (This why at ClearLogic we prepare for them in our clients’ portfolios and financial plans and work with our clients so that they are prepared for them not just financially, but also mentally and emotionally.)

SEE MORE

We at ClearLogic often tell our client “don’t try to save a buck; focus on how you want to live your remaining year”. Now there’s scientific research that shows spending a buck here and there to save time improves happiness.

A study in the Proceedings of the National Academy of Sciences suggest that spending money to save time may reduce stress about the limited time in the day, thereby improving happiness. Over 5,000 people in the United States, Denmark, Canada and the Netherlands were surveyed in 2 rounds on well-being and timesaving purchases, such as ordering takeout food, taking a cab, hiring household help or paying someone to run an errand. 28 percent in the first round and 50% in the second who made such purchases reported greater life satisfaction than those who did not. Despite its benefits, the practice of buying time is not as popular as one might expect, they found. Even among more than 800 Dutch millionaires surveyed, all of whom surely could afford to do so, only a slight majority spent money on timesaving tasks.

While a Protestant work ethic that values being busy or guilt over paying someone for a task that people could easily do themselves, the data now shows a buck here and there to save time especially on dreadful tasks provides significant happiness. We recommend reading more about the study in the fun article in the New York Times.

SEE MORE

Significant tax savings are possible from deductions for assisted living facilities, nursing homes, and continuing care retirement communities. Taxpayers can deduct medical and dental expenses for the taxpayer, the taxpayer’s spouse, or relatives the taxpayer supports that are more than 10 percent of their adjusted gross income – including long-term-care expenses for chronically ill people even in a nursing home.

The determination of “chronically ill” must be made by a licensed health care practitioner who must certify the resident as unable to perform at least two activities of daily living for at least 90 days due to a loss of functional capacity. Severely cognitively impaired individuals requiring substantial supervision, such as those with Alzheimer’s disease, also qualify as chronically ill. If the taxpayer does not qualify as chronically ill by reason of being able to perform two or more of the activities of daily living, a portion of the cost of the stay at the assisted living facility is still deductible.

It is important to discuss and plan for long-term-care costs as well as available tax benefits and insurance options as part of one’s annual financial review. Having the right documentation in advance to take advantage of all tax benefits is equally important. We recommend reading more details about the tax benefits in an excellent article on the subject. (ClearLogic guides clients with the financial/tax, logistical, and even emotional aspects of long-term care and medical costs as part of handling “all things financial” for clients.)

SEE MORE

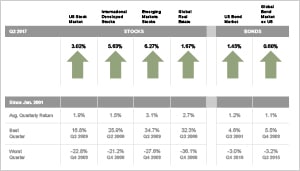

Global stock markets again rose during the second quarter of 2017. Additionally, both US and international bond markets were up, making the second quarter of 2017 positive across the board. Last quarter, we noted that international stock markets outperformed US stock markets, reversing a trend we had seen over the past few years. The reversal continued this quarter with international stocks returning about double what the US stock market returned.

Of ClearLogic’s 10 Investment Principles for long-term conservative growth, most at play this quarter were “look beyond the headings”, “practice smart diversification”, and “let markets work for you”.

SEE MORE