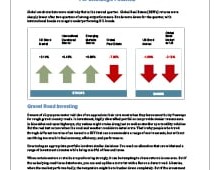

Despite another volatile quarter, capped by the Brexit decision in late June, stock and bond markets once again had a positive quarter. In fact, the chart below looks almost identical to the same chart in the first quarter. Global Real Estate outperformed all other asset classes again in the second quarter, and International Developed stocks were the only asset class to provide negative returns.

READ MORE